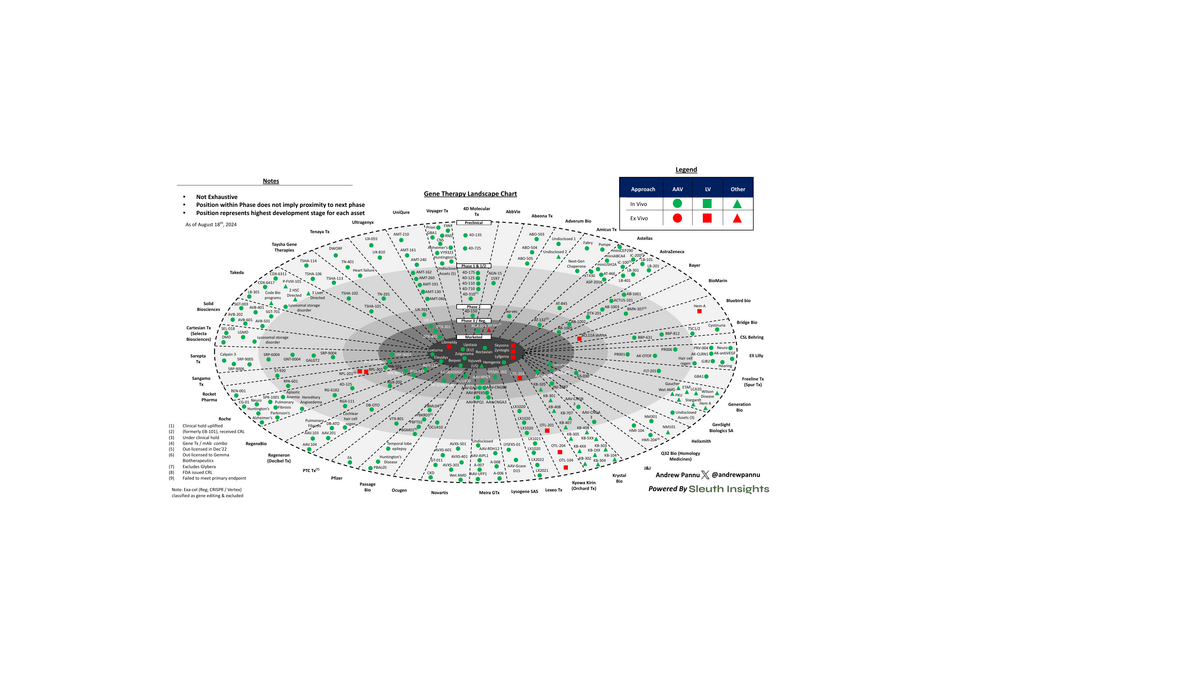

Gene Therapy Landscape: 42 Companies, 200+ Assets

42 companies charted across 450+ gene therapy programs. 11 approvals across 10 indications, with 4 in the last 18 months.

Download the Visual

Pulled together 42 companies and charted the preclinical and clinical assets of each, segmented by approach and vector

Some takeaways:

The analysis above is just a sample of the overall activity in the space - there are 450+ programs across 200+ companies, the vast majority of which are very early (~60% are preclinical and majority of clinical assets are in Ph 1/2). This also excludes gene editing approaches.

With that said, there is clear momentum in the space: 11 gene therapies across 10 indications have been approved in the US, with 11 approved globally. 4 of these therapies were approved in the last 18 months indicative of early investments in the space starting to bear fruit

Gene therapy works by correcting, removing or adding external genetic material that does NOT integrate into the patient's genome at a specific loci to treat disease. Delivery of this genetic payload is key and right now >70% of assets are AAV-mediated (LV is 2nd with ~10-15%)

The hundreds of programs in this space touch a fairly diverse range of therapeutic areas. The most common are neurology (~33%), metabolic (~20%) and ophthalmology (~15%), but therapies are being deployed across the board

From a capital markets perspective, the space (along with many areas of biotech) reached a zenith in 2020-2021, and has since gone through a long winter, with fewer IPOs, follow-on financings and acquisitions. As a rule of thumb, when a space is early, Pharma reaches for BD first

The rush of recent approvals has shifted the focus from clinical proof-of-concept / regulatory hurdles towards commercial performance. It's no secret these drugs are expensive, with each new approval often setting a new record for highest priced drug

In 2023, approved drugs generated ~$2B in global sales, certainly boosted by the # of recent approvals. If sell-side estimates hold, current and forthcoming approved assets could generate >$10-15B by the end of the decade

It's not all up and to the right though. BioMarin's Roctavian has treated just a handful of patients since receiving EMA and FDA approval in 2022 and 2023 respectively, eeking out just $3.5M in sales in 2023. Barring a dramatic turnaround, the asset will likely be deprioritized

Looking ahead, there are several assets worth watching that are at or near regulatory approval decisions:

- RP-L102 (Rocket Pharma) - received CRL

- RGX-121 (Regenxbio) - 2H'24

- Upstaza (PTC) - Nov'24

- Pz-cel (Abeona) - received CRL

- SB-525 (Pfizer / Sangamo) - 2025