All articles

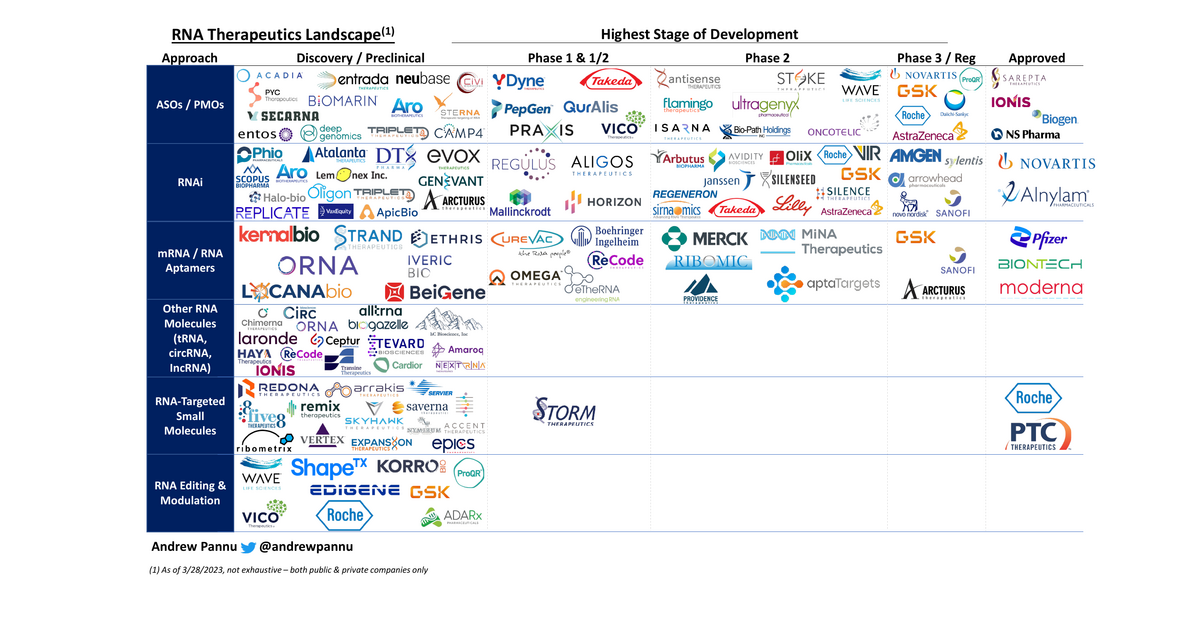

RNA Therapeutics Market Map: 124 Companies

124 companies across 350+ programs. 16 RNA drugs approved, projected to exceed $20B in annual sales by 2030.

March 28, 2023

Download the Visual

124 companies are segmented by approach and highest stage of development

Some takeaways:

- The space is exploding - 350+ total programs are targeting a diverse set of TAs. The most common are neuromuscular disorders (~20%), oncology (~18%), infectious disease (~14%) and neurology (~13%)

- By dev stage: ~50% PC, ~38% Ph1/2, ~8% Ph3 and ~4% Mktd.

- RNA therapies cover a range of mechanisms, molecule types and therapeutic aims. I've classified the space into three broad groups:

(1) RNA-based therapeutics

(1a): Endogenous RNA targeting (i.e. ASOs / PMOs, RNAi)

(1b): Direct RNA therapeutics (i.e. mRNA, RNA aptamers)

(1c): Other RNA molecules (i.e. tRNA, circRNA, IncRNA, etc.)

(2) RNA-targeted small molecules

(3) RNA sequence & structure modulation (i.e. CRISPR, ADAR, etc.)

- 16 RNA drugs have been FDA approved, with 2022 sales totaling $3.6B (excl. >$56B from mRNA COVID-19 vaccines). Sell-side estimates assume >$20B in annual sales by 2030, driven by new launches & more prevalent indications

- RNA-based therapeutics offer several advantages over other modalities:

- Potential for rapid development

- Able to treat a broad range of diseases that may be "undruggable

- Can be personalized (ultimately to 1 of 1 drugs)

- Rapid cellular utilization vs. DNA therapies

- However, there are some drawbacks:

- RNA is usually rapidly eliminated by immune system (part of the reason Moderna pivoted to vaccines), thus requiring several doses & inducing potential immunogenicity

- Delivery is a challenge due to instability & tissue / cell uptake

- With that said, many companies are trialing novel delivery, dosing & design approaches to enhance stability, improve druggability and reduce immunogenicity. Next-gen approaches include targeting RNA with small molecules, protein replacement, "base editing for RNA" & much more

- Deal flow in this space has been robust, driven by a healthy mix of players: big pharma, mid-caps with deep pipelines and innovative biotechs + strong investor appetite

A few stats:

- 50+ licensing + collaboration deals over past few years, totaling >$40B of disclosed value

- >$10B public financing since 2018

- ~$17B in M&A deal value since 2019, primarily driven by Novartis / Medicines Co. ($9.7B), Sanofi / TranslateBio ($3.2B) and Novo Nordisk / Dicerna ($3.3B)

- On the manufacturing & supply chain side, RNA therapies are a balancing act between reproducibility & stability. Manufacturing is generally cost-effective, scalable and reproducible (as we saw with mRNA vaccine rollouts). However, low stability means cold storage may be required

- Multiple companies are developing modular platform technologies that can be theoretically applied to a range of diseases via proven chemistry. Successful lead programs could thus "de-risk" the entire pipeline. How much belief investors / regulators have here is an open question