Biotech Has a Consolidation Problem

Biotech has a consolidation problem. Far too many companies are chasing similar innovations with too few buyers.

Download the Visual

+ other insights from an analysis of >$1B biopharma M&A deals since 2019:

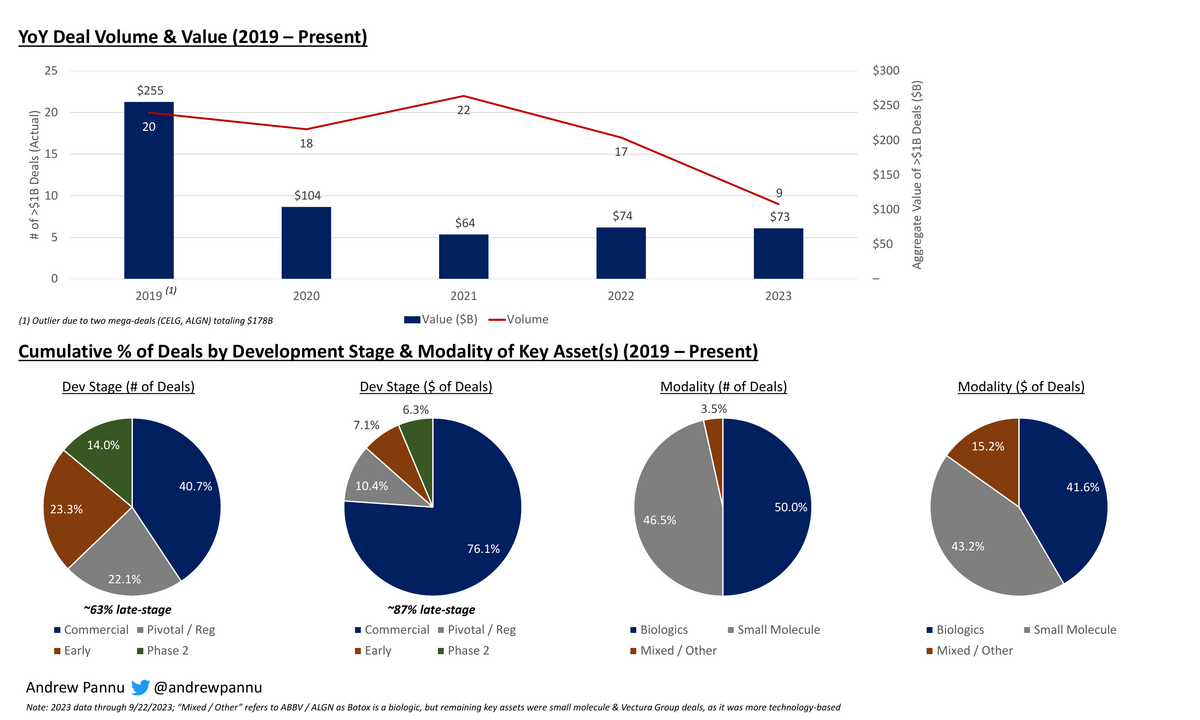

Exhibit 1: YoY deal volume / value + % of deals by development stage & modality

We've seen a noticeable dip in >$1B deals this year, although deal value is in-line (~$75B) with the past few years

The majority (~63%) of deals have been for companies with approved or pivotal / registrational stage assets and the vast majority (~87%) of $ have been allocated here

This makes sense given pharma's recurring need to replace at-risk LOE revenue, which is particularly pronounced over the next few years.

Exhibit 2: Major pharma LOE to 2028

The implication for biotech is not to expect a huge takeout based on platform value or early-stage assets - stellar pivotal data and (increasingly) strong launches are needed to get deals done. The winners must build early conviction on differentiated assets, navigate volatile markets to fund pivotal trials and keep commercial scale-up in mind—a challenging balance

Additionally, while M&A has long been considered the lifeblood of the industry, immense capital inflows over the past few years supported the creation of a record number of biotechs - far too many to be consolidated by pharma

Many that make it to the other side will still find no buyers, which is problematic if their asset(s) can't generate enough cash flow to sustain independence. Pharma will always bias towards assets with >$1B peak sales potential, so those in "no man's land" of $500M - $1B can be passed over unless they fit perfectly with existing commercial infrastructure

We may see a few of these companies merge in the absence of pharma buyouts, essentially creating enough scale by combining smaller assets to support an independent commercial-stage company

The historical mix of biologics vs. small molecules has ebbed & flowed each year but cumulatively is ~50/50. Recent drug approvals have tilted more toward biologics, and the IRA has further incentivized their development, so in the future, we might expect the ratio to shift in that direction

Exhibit 3: % TA Mix

As expected, oncology & immunology are the most common TAs, followed by rare disease and CNS. These areas benefit from assets that can be used across multiple indications & favorable reimbursement structures + unmet need

We typically see at least 1 mega-deal (>$20B) every year:

2023: $SGEN

2022: $HZNP

2021: None

2020: ALXN & IMMU

2019: CELG and ALGN

Exhibit 4: Future potential acquisition / merger targets

Looking ahead, companies in priority TAs with late-stage or commercial assets that could garner M&A interest are flagged. The median market cap is ~$3B, which aligns with pharma's stated preference for manageable bolt-ons rather than mega-mergers. As noted above, it's also possible some of these names merge