CDK4/6 Competition in mER+ Breast Cancer

CDK4/6 competition in mER+ breast cancer is a case study in how flawless execution separates winners from clinically equivalent competitors.

Download the Visual

The competition amongst CDK4/6 inhibitors within mER+ breast cancer is an interesting case study on how flawless execution is needed in today's markets.

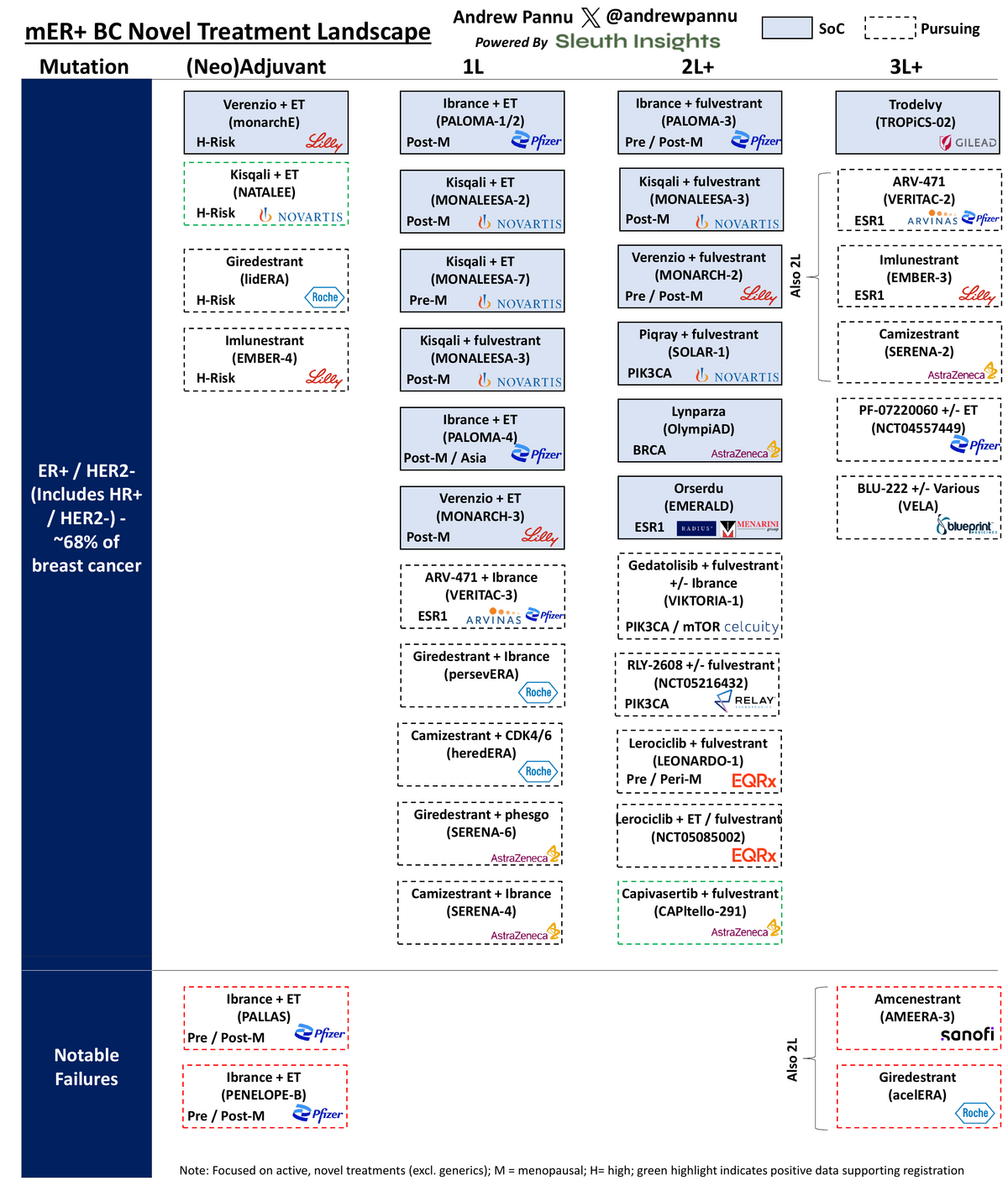

Exhibit 1: mER+ Breast Cancer Treatment Landscape

First, a brief history of this space:

- ~65-70% of all breast cancers are ER+

- Traditionally treated with endocrine hormone therapy, which had issues with durability

- SERDs (Faslodex) offered a welcome alternative but had dosing inconveniences (monthly intramuscular injections + inability to offer high dosing)

- CDK4/6 class was huge breakthrough - now the de facto 1L and, depending on patient profile, adjuvant / 2L as well

- 2L+ is more wide open, with exception of those with PIK3CA mutations

- Oral SERDs competing in 2L+, although the class has been hit with numerous late-stage clinical failures; a few winners have emerged, particularly those with smart trial design enriching for ESR1m+ subgroups (i.e. Menarini's EMERALD)

It will be interesting to monitor payor reception of oral SERDs pending final readouts - some differentiation beyond convenience of oral dosing might be needed to justify reimbursement and uptake

Going back to CDK4/6 competition, Pfizer's Ibrance, Novartis' Kisqali and Lilly's Verenzio are competing for differentiation across:

- OS benefit: Ibrance (PALOMA) missed, Verenzio (MONARCH-2) / Kisqali (MONALEESA-2/3) hit

- Setting: Verenzio (monarchE) & Kisqali (NATALEE) hit in adjuvant, unlocking >130K additional patients

- Dosing convenience: Verenzio is continuous vs. others are 3 weeks on / 1 off

- Safety profile: around neutropenia, gastro tox, cardiac tox and others

- Pricing: Kisqali is ~20% cheaper than Ibrance & has a co-pack with letrozole

- CNS penetration: Verenzio has high BBB penetrability

Pfizer's 2-year first-to-market advantage allowed it to capture early adopters - of the $10.3B in global CDK4/6 sales (LTM Q3'22), Pfizer captured 48% ($4.9B), down from 58% in FY22

With the caveat that forecasts' are always wrong, current projections show that lead continuing to get erased, driven by disappointing long-term OS data and failures in the adjuvant setting (PALLAS, PENELOPE-B). Pfizer's share of new US scripts and overall TRx has trended down QoQ since at least late 2022, although patient & physician familiarity may offer a buffer to slow declines.

Exhibit 2: CDK 4/6 inhibitor class sales projections

Instead, Lilly's third-to-market Verenzio is expected to be the top-selling asset, driven by success in the adjuvant setting, continuous dosing and a better safety profile around neutropenia.

That this type of competition keeps companies on their toes to continuously generate compelling new data is a win for patients, but it is remarkable how little room for error there is for sponsors. We even see it above at a class level above with SERDs and now oral SERDs - any weakness in safety, dosing or trial design can sink an asset's potential, even if it is more effective than the current SoC.