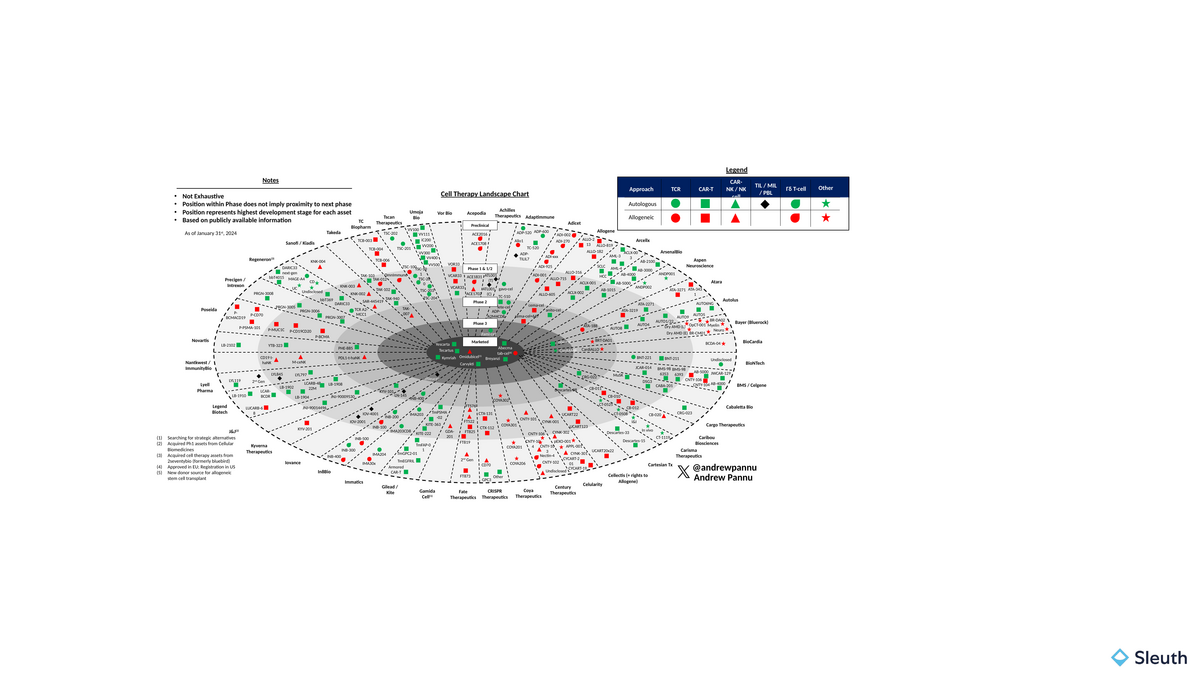

Cell Therapy Landscape: 45 Companies, 400+ Programs

Is the best yet to come for cell therapy?

Download the Visual

Is the best yet to come for cell therapy?

I pulled together 45 companies in the space and charted the preclinical and clinical assets of each, segmented by cell source and modality

Exhibit 1: Cell Therapy Landscape

Some thoughts:

The above is just a snapshot - an attempt to capture key pivotal programs while also flagging the diversity of novel approaches. If we zoom out, it's clear that the space is still in hypergrowth:

- >150 companies pursuing 650+ programs across 100s of clinical trials

- >$200B in cumulative public / private investment since 2014

- 6 FDA approved CAR-T therapies with >$5B in aggregate sales

And while there's been plenty of warranted criticism about whether the space is overfunded, yesterday's Regeneron announcement shows that Pharma still sees a lot of upside - both within oncology, and within emerging efforts in I&I / CNS

Historically, we've seen that enthusiasm play out via BD deals - transformative M&A has been missing from the space since 2017-18 (Kite, Juno)

Exhibit 2: IPO and M&A Activity from 2013-2023

IMO there's a few reasons for this:

(1) The pace of innovation creates shiny object syndrome, so why not wait for the dust to settle and place smaller bets in the interim

(2) We're approaching 7 years since the first FDA approval, and Pharma is still facing supply chain woes, proving the difficulty in scaling manufacturing, QC and distribution for these medicines (and these investments don't transfer well if you pivot)

(3) A higher interest rate world and >$200B in upcoming LOEs means Pharma is much more focused on acquisitions that drive near-term revenue

(4) Access to easy capital from 2019-2021 led to an explosion of IPOs as public market demand for innovative, earlier-stage companies peaked

(5) Competition from alternatives like bsAbs may impact the ability to penetrate 1L setting

These points will combine to lead to some painful drawdowns - more companies will continue a theme we saw the last 2 years and announce strategic alternatives, wind down programs or consolidate

So are the best days behind us? I don't think so.

The challenges are real, but keep in mind the rate of progress: 11 years from first trial to FDA approval (2006 --> 2017) and <20 years from that point to today. Using mAbs as a historical analog, we're just entering the first inflection in value and tracking well ahead at the same time point

Exhibit 3: Antibody Dev Over Time (source: Lu et al. (2020))

The amount of intellectual and financial capital locked up in this space almost guarantees we'll see groundbreaking milestones - which perhaps we're already seeing with (very early) data indicating outstanding CAR-T effectiveness in autoimmune diseases, for which most patients relapse on current treatments and there are no cures

Ultimately, cell therapy's potential as a one-time life changing therapy ensures it will continue to capture our attention (and investment) moving forward, even as we work through growing pains