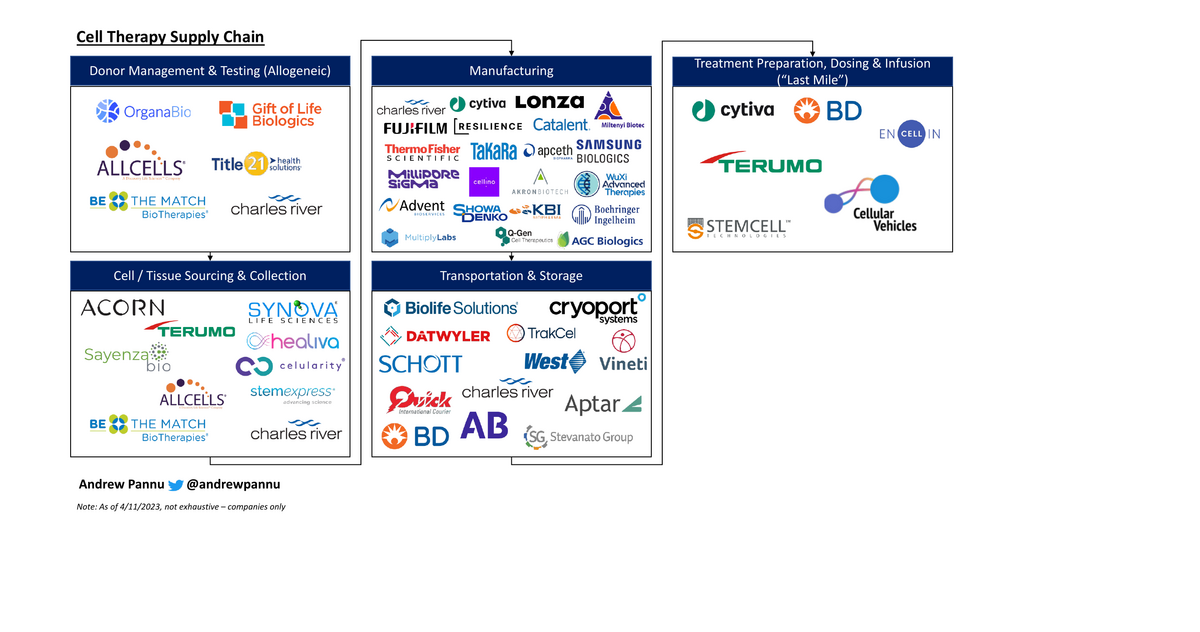

Cell Therapy Supply Chain Market Map

49 companies mapped across the vein-to-vein supply chain. Manufacturing complexity remains the binding constraint.

Download the Visual

Segmented 49 companies by stage throughout this vein-to-vein process

Some thoughts on the complexity of bringing these medicines to patients:

- Cell therapy development followed a launch first, ask questions later approach:

Clinical development of first-generation therapies outpaced efforts to establish robust manufacturing processes, leading to a wave of issues at launch for Kymriah / Yescarta

- The step-up to commercial manufacturing & delivery from small-batch trials is huge

Companies can get away with more manual processes in the latter, but maintaining the viability & functionality of cells at scale requires better automation, analytics and a mature supply chain

- As automation accelerates, demand for multidisciplinary roles is increasing too. Our industry needs more data and computer scientists, but the competition for these individuals is intense, especially when biopharma pays less than equivalent tech roles

Keeping good people is hard

- Variability in starting material due to process / patient nuances significantly complicates the entire supply chain. There is a delicate balance between ensuring adequate cell numbers & moving as fast as possible to avoid disease progression

More automation is key here as well

- As commercial & clinical demand skyrockets and larger indications are coming into focus, there is a lot of ongoing effort to better industrialize the supply chain

Shortages are particularly apparent for the approved BCMA CAR-Ts

- Uncertainty over clinical readouts & a vicious talent war has historically tempered companies moving towards in-house manufacturing

The most common playbook is to rely on CDMOs for early development and begin transitioning towards more in-house work with later-stage assets

- Established manufacturers & CDMOs are doubling down on the space to address demand, with huge investments over the past few years

Given the tighter funding environment, it's likely companies rely on CDMOs more moving forward, to preserve capital & focus on core

- Allogeneic therapies could allow for a more traditional manufacturing model, with simpler collection, storage & economics.

However, clinical success has been limited, tempering near-term expectations

- To maintain cell fitness, cell therapies need to be stabilized by cryogenic preservation or refrigeration during transportation & storage

Similar to CDMOs, third parties in this space are ramping up investment given the exploding demand & massive pipeline

- "Last mile" delivery to the patient is a critical and often underappreciated component. We'll need to expand beyond inpatient infusions at academic centers and towards outpatient clinics and community care settings

That will require better hospital infrastructure & training