The China Biotech Partnership Funnel

Everyone evaluating China biotech partnerships for US/EU development is asking the wrong question.

Download the Visual

Everyone evaluating China biotech partnerships for US/EU development is asking the wrong question.

BD teams are hunting for breakthrough science, novel targets, and pristine IP. Meanwhile, the assets most likely to close deals in the next 18 months are biosimilars and follow-ons from the same handful of experienced sponsors.

Why? CMC transferability has become the rate-limiting step, not clinical differentiation.

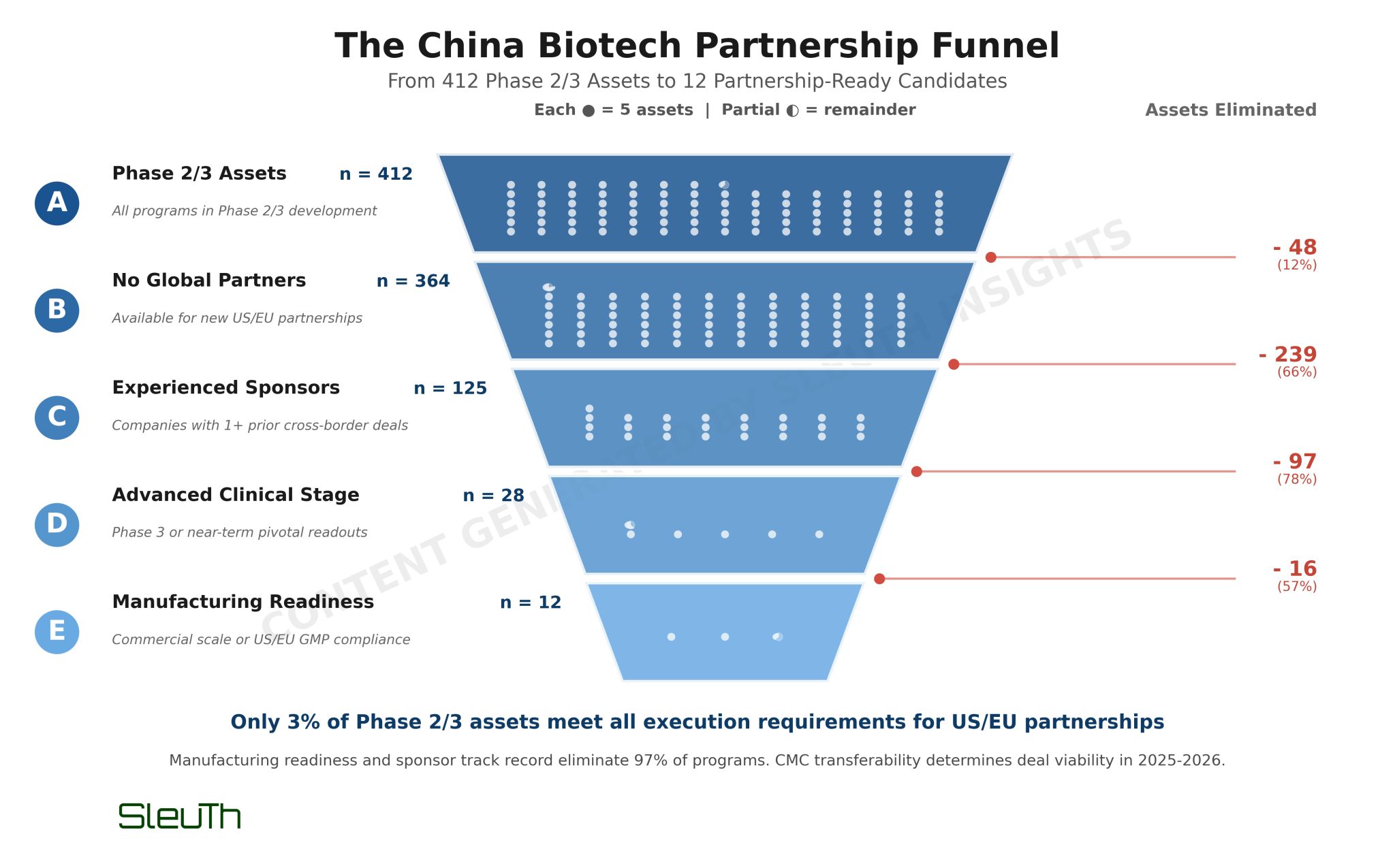

I used Sleuth to analyze 412 Phase 2/3 China-developed assets across clinical, IP, CMC, and geopolitical dimensions. The data contradicts conventional partnering wisdom.

Historical deal analysis shows sponsors with 5+ prior cross-border transactions command median upfronts of $60M for Phase 2 assets - but only 35% of Phase 2/3 assets come from sponsors with this experience. More importantly, less than 1% have achieved commercial-scale, export-ready manufacturing with Western GMP compliance.

This creates a severe funnel. Of 412 Phase 2/3 assets, only 66 meet the minimum bar: advanced clinical stage, no existing global partners, and sponsors with meaningful deal experience. Layer on CMC readiness (commercial-scale capacity with US/EU GMP) and that drops to single digits.

The assets clearing this bar aren't cutting-edge science. They're biosimilar anti-PD1s, follow-on ADCs, and reformulated small molecules from Hengrui, Bio-Thera, and CSPC. These sponsors have transferred manufacturing successfully before, maintain dual compliance, and can navigate FDA CMC packages without starting from scratch.

Meanwhile, dozens of more innovative programs (novel IO combinations, differentiated cell therapies, first-in-class small molecules) remain stranded at clinical supply scale with China-only GMP and zero Western CDMO transfer experience. The tech transfer risk alone adds 18-24 months, and with geopolitical uncertainty already extending diligence by 6-9 months, that's functionally disqualifying.

The implication for BD strategy is clear: if your mandate is to close China deals in 2025-2026, you're shopping from maybe 20-30 realistic candidates, most clinically undifferentiated but operationally de-risked. The breakthrough science you want is either already partnered or won't be ready for US/EU tech transfer until 2027+.

For biotech executives, this is a forcing function. Western GMP compliance, commercial-scale manufacturing, and demonstrated tech transfer capability need to be in place before Phase 2 topline data, not after. Otherwise, you're competing with 400 other assets that will never attract a credible bid.

The window for opportunistic partnerships is narrow. Assets with 2025-2026 readouts, experienced sponsors, and manufacturing infrastructure will command premiums despite being unremarkable.