Drugs Likely Selected for IRA Price Negotiation in 2027

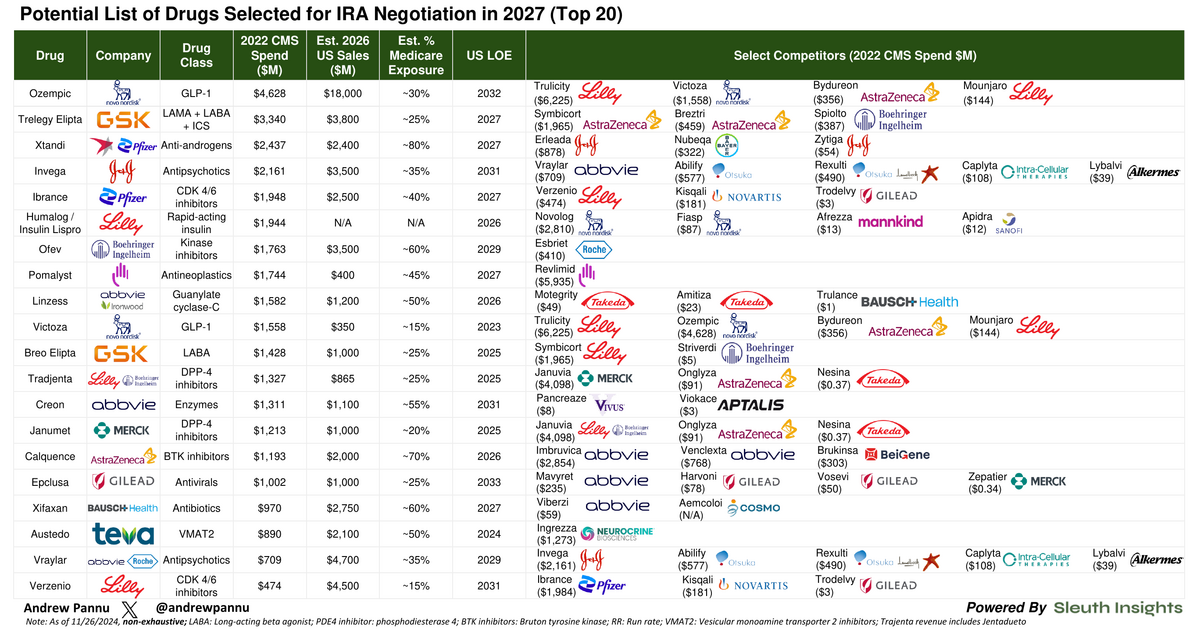

The top 20 drugs that could be selected for Medicare price negotiation in 2027. 15 will be chosen.

Download the Visual

The top 20 possibilities (15 will be selected) with data on 2022 CMS Spend, 2026E sales, % Medicare exposure and select competitors that could experience knock-on effects

Additional takeaways:

Given we're only in round 2 of the IRA selection process, a lot of potential drugs are expected to have generic entry pressure around 2027 anyways, so the overall impact might not be that bad (as was the case in 2026)

Selected drugs will be revealed by Feb 1st, 2025

Whether we see spillover pressure for competitive drugs is highly dependent on whether the negotiated drug is a credible substitute

Given that, one thing to watch for moving forward is whether late-movers initiate H2H trials against market leaders earlier on

The goal would be to position themselves favorably should that market leader get selected by CMS

For example, BeiGene's Brukinsa showed H2H superiority vs. Imbruvica (selected last year) in r/r CLL (ALPINE). Mgmt. was thus confident the indirect impact would be minimal

It'll also be worth monitoring how these publicly disclosed prices will impact negotiations with commercial payors

At a minimum, this process gives payors a lot of new leverage to extract additional rebates (including cross-portfolio & with competitors)

Once these drugs are selected, it'll be interesting to see where negotiated prices end up for drugs within Medicare's 6 protected classes (i.e. oncology, neuropsych, some I&I) vs. all others.

For drugs outside these classes, selection can end up being a muted event

That's because formulary placement is not mandated, and thus drugs compete for placement via a host of methods, including aggressive rebating. This is especially true when competition is high, as is the case in diabetes or CV, where rebates can already be 50-80%

That's not to say CMS can't cut even deeper - they have broad latitude to do so under the law - but there might be limited room. Last year the average discount was ~22% off net spend and drugs in protected classes were treated fairly favorably, with pricing near the ceiling

Details from round 1 indicate that CMS will negotiate in good faith - it accepted 4 counteroffers from companies last year and didn't look to be overly aggressive

That could end up being unique to round 1 just to ensure a smooth kickoff, so it's worth watching if the trend holds

Ultimately, Medicare spend from 11/1/23 - 10/31/24, timing of Gx entry and edge case handling (i.e. rare disease exclusion) will be key

It's also worth monitoring how a new administration impacts IRA-related policy