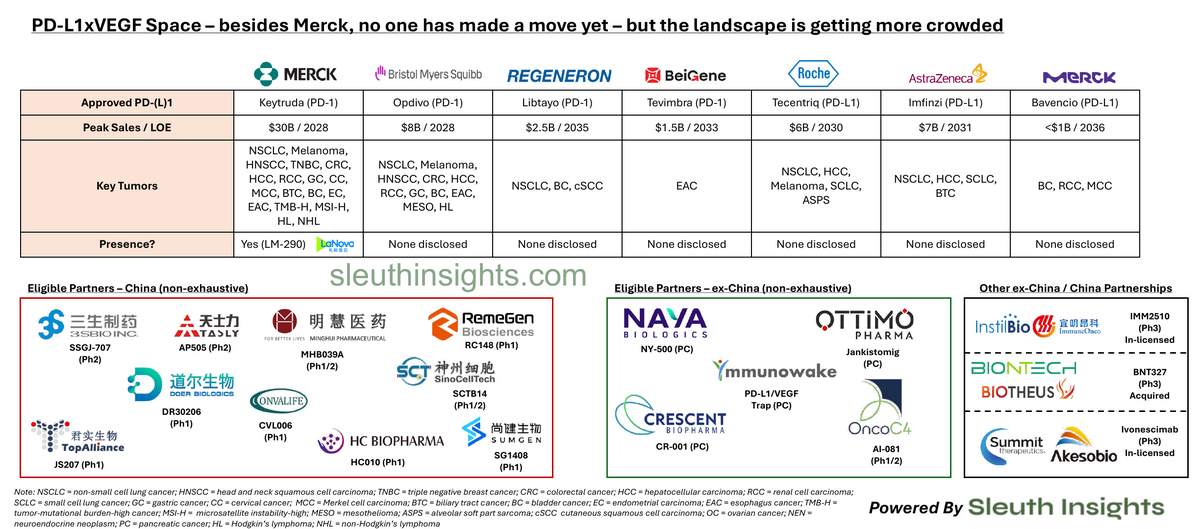

PD-L1 x VEGF Market Overview: Why Only Merck Has Moved

Besides Merck, no pharma with an approved PD-(L)1 inhibitor has made a move yet. The early-stage landscape is getting crowded.

Download the Visual

PD-L1 x VEGF landscape analysis

Besides Merck, no pharma with an approved PD-(L)1 inhibitor has made a move yet, but the early-stage landscape is getting more crowded.

Meanwhile, the entire industry is awaiting OS results for HARMONi-2 in 2025.

Some thoughts on this space:

Key context: this space is hot because in Sep'24, Summit Therapeutics and Akeso published results showing ivonescimab (PD-1 x VEGF) reduced the risk of disease progression in 1L PD-L1+ NSCLC by 49% vs. Keytruda, the undmisputed king of this treatment setting (HARMONi-2 study)

While a big win, critical questions remain open:

- HARMONi-2 was entirely conducted in Chinese patients - will it transfer to a global population? (HARMONi-7 is a global Ph3 that aims to answer this)

- Extending survival (OS) is the key endpoint to watch - will the impressive mPFS results translate over? (We'll find out in mid-2025)

- A win against Keytruda mono is a good start, but in many tumors frontline SoC is actually Keytruda + chemotherapy (HARMONi-3 will begin testing this in 1L squamous NSCLC)

The degree and durability of separation in the HARMONi-2 PFS curve does bode well for a stat sig OS result - mOS and mPFS are historically well correlated in 1L IO trials. And Asian vs. Non-Asian outcome differences tend to be more pronounced in mutation-driven cancers such as EGFR

Regardless, a few companies haven't decided to wait for more data to emerge (and potentially drive prices higher), instead following Summit's playbook and in-licensing competitive assets directly from China:

- Merck in-licensing LM-299 from LaNova ($588M upfront)

- BioNTech acquiring partner Biotheus ($800M upfront) for BNT327

- While earlier, Instil in-licensing IMM2510 ($50M upfront)

- Merck is also collaborating with Exelixis' zanza (VEGF TKI) as a hedge

Looking at the broader landscape, you have to imagine that every Pharma with a blockbuster PD-(L)1 asset is looking closely at this space. It presents a strong LCM add-on to their existing portfolio, and they can leverage their prior experience running large, multi-tumor clinical development programs to quickly catch up to the market leaders

And it's a landscape dominated by Chinese biotech companies right now - so far every major US company has gone there to find their asset, and the vast majority of eligible partners are based there. This echoes a theme we've seen in other modalities (such as T-cell engagers). It will be interesting to track US venture funding into this space - will VCs fund US-based competitors if the market has shown a willingness to source more advanced (and de-risked) assets directly from China?