How Big Pharma Valuations Trend Before and After Major LOEs

How have big pharma valuations trended around the biggest LOEs the industry has seen? Surprisingly, pretty well.

Download the Visual

How have big pharma valuations trended before and after some of the biggest LOEs the industry has seen? Surprisingly, pretty well.

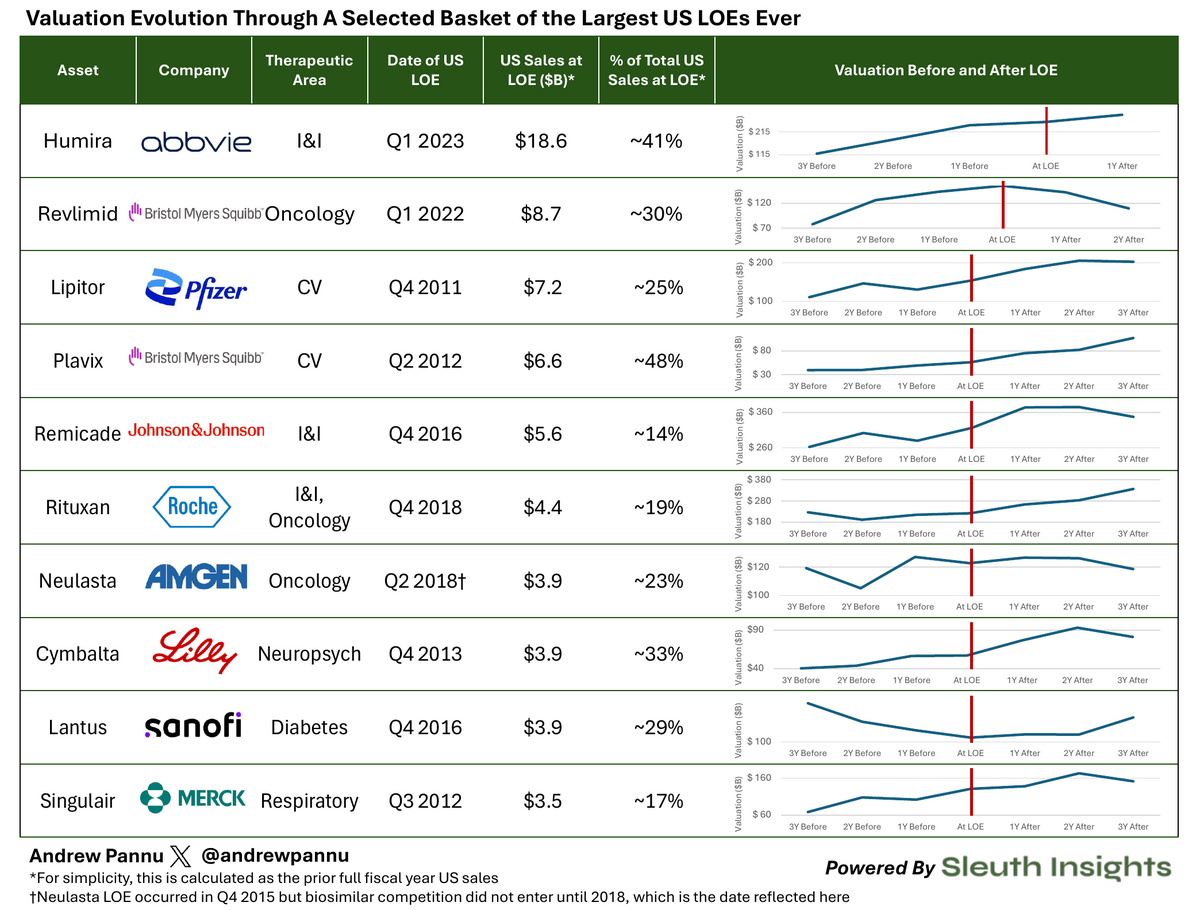

Exhibit 1: Largest US LOEs and Company Valuation Performance

First, some quick stats. On average, these drugs represented ~28% of US sales just prior to LOE. All were in the hands of big pharma and unsurprisingly, most were within oncology, I&I or cardiovascular diseases

When companies did take a hit, it tended to be about a year prior to the LOE. However, this is not a rule - there were several instances of company valuations expanding through the LOE and beyond

With the exception of Sanofi, company valuations expanded in the year after the LOE, with performance more split in Y2 between growth / flat trajectory / slight decline

On the surface, this result feels counterintuitive. LOEs precipitate the loss of billions of dollars of revenue - how is it that these companies tend to emerge largely unscathed? A few ideas (please add your own in the comments!):

- Companies are not blind to their own LOEs and thus they spend a considerable amount of effort and resources addressing future shortfalls well in advance through M&A, BD and internal R&D. In theory, these should adequately replenish the pipeline to provide future growth opportunities that offset the revenue hit from the LOE

AbbVie is a great recent example, with Skyrizi and Rinvoq now estimated to deliver a combined $27B by 2027, which actually outpaces Humira's peak sales of ~$20B. After the largest LOE ever, AbbVie will likely be back to growth in 2025

In the run up to big LOEs, companies also smartly use every interaction they have with investors to redirect attention to their pipeline / M&A capacity and guide the narrative towards continued growth

- While there are clearly exceptions, it's possible companies are simply oversold in the run-up to the LOE, such that by the time it happens, most of the value has already been extracted. At that point, the story can change back to one of future growth, particularly as the base from which the company has to grow has likely reset a few years

- Lastly, it's possible that historical data is not a useful barometer as the size of LOEs this decade will dwarf anything we've seen before (except Humira), headlined by the $30B Keytruda LOE in 2028. The below graphic captures some other notable upcoming LOEs:

Exhibit 2: Notable US LOEs Through 2028