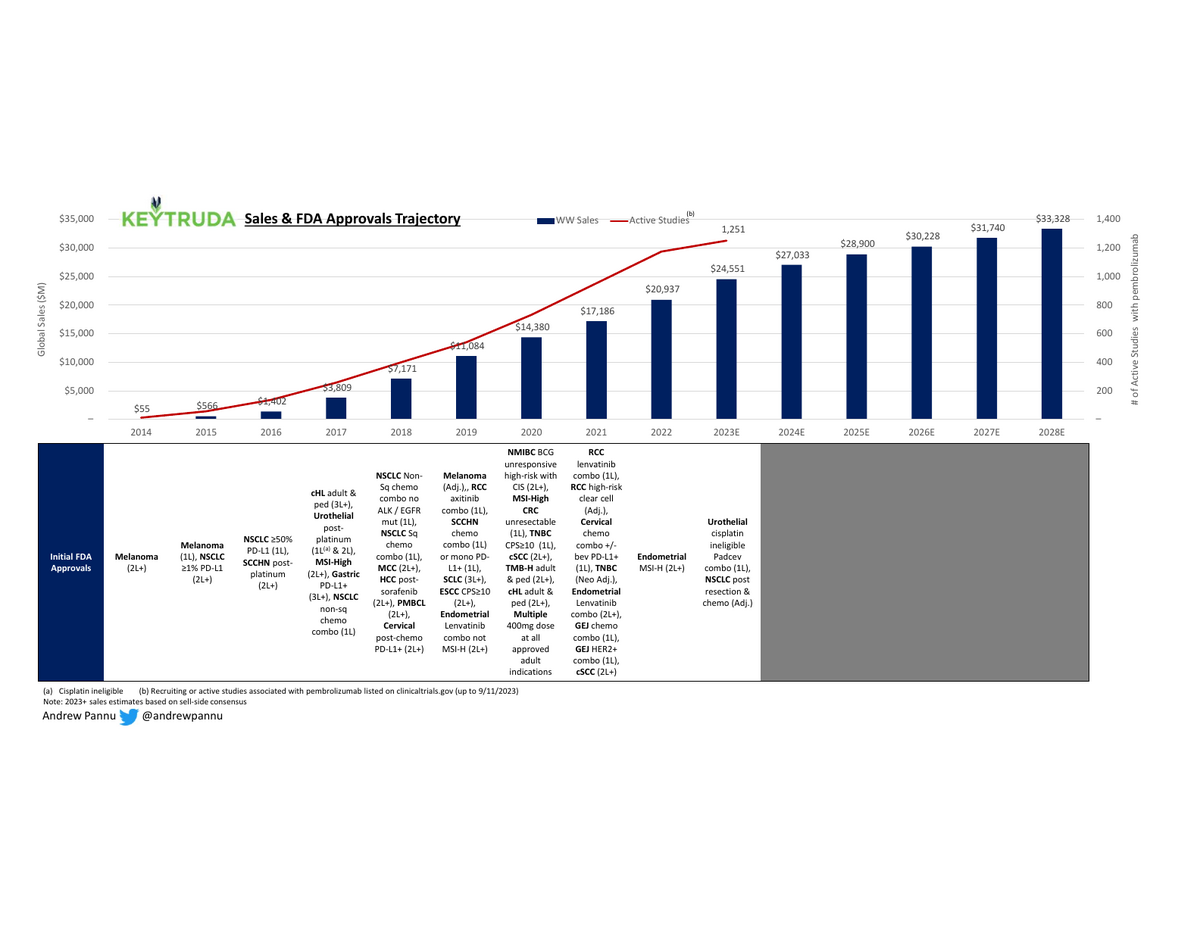

How Merck Built a Blockbuster With Keytruda

39 FDA approvals across 16 tumor types on the road to >$30B in annual sales by 2028.

Download the Visual

39 FDA approvals across 16 tumor & 2 tumor-agnostic indications on the road to an estimated >$30B in annual sales by 2028

And expect more coming: Merck is running >1K pembrolizumab trials (incl. 400+ combo trials & 80+ registrational studies) in 30+ tumor types

All of that is contributing to likely the largest LOE cliff ever beginning around 2028 (the same year Keytruda is eligible for Medicare negotiation under the IRA).

Merck is developing a sub-Q formulation that might blunt some of the LOE impact if they manage to shift a proportion of patients over from IV infusions. The justification for doing so would be improvements in patient QoL (less invasive & time-consuming, shorter hospital stays for high-risk patients, greater access), but it's likely that >80% of revenues would be at-risk from biosimilars, given the cost & reimbursement benefit of opting for the IV formulation

A sub-Q formulation does involve adding a new compound (hyaluronidase), so it's assumed (but not yet confirmed) that CMS would treat this as a new drug and thus restart the clock for direct negotiation

Keytruda represents the most successful example of the oncology strategy of starting in late-line patients with few options and "moving up" to adjuvant / 1L over time. With the new rules under the IRA starting the exclusivity clock at first approval, this approach makes less sense, since the adjuvant & 1L settings are multiple times larger than the metastatic setting. Companies may opt to run parallel studies in both settings to sync approval or start with earlier settings. Of course, the bar is much higher upfront, so this strategy does carry a lot more R&D risk.

Like so many other drugs, the success of Keytruda is full of serendipity. It was discovered accidentally by scientists looking to stimulate (not inhibit) PD-1 and was repeatedly de-prioritized through multiple acquisitions (Organon to Schering in 2007 to Merck in 2009) given how (up to that point) nothing in immuno-oncology worked well. Only after BMS published promising Phase 3 results for Yervoy (a CTLA4 inhibitor) & rumors of great results for an earlier-stage PD-1 inhibitor (Opdivo) leaked did Merck hastily prioritize development

Despite being years behind BMS, Merck benefited from (1) the then-new Breakthrough Designation FDA pathway and (2) the decision to rely on the PD-L1 biomarker as a way to stratify patients & focus on those most likely to respond. While risky (BMS opted to develop without a biomarker and thus could target a broader label & avoid the friction of needing to get tested to use a drug), it ultimately helped close the gap in NSCLC as Opdivo failed a key 1L trial in 2016. It was a lead Merck would never give up.